{kind=link}

Immense concentration continues apace in the cloud industry, with hyperscalers expected to comprise 67% of global datacentre capacity by 2031, or 14 times the capacity they had in 2018. Back then, enterprise datacentres accounted for 56% of all datacentre capacity.

That’s according to figures from US-headquartered research organisation Synergy Research Group, which says artificial intelligence (AI) is driving huge and accelerated growth, with hyperscaler capacity expected to double in the next three years.

By the fourth quarter of 2025, Synergy found that hyperscaler-operated datacentres accounted for 1,360 of total sites and 48% of worldwide capacity. Datacentres built by hyperscalers form the bulk of that capacity – 60% of it – with the remaining capacity leased.

Non-hyperscale colocation capacity accounts for 20% of current totals, while enterprise datacentres account for 32%.

Synergy expects hyperscaler datacentre capacity to comprise 67% of all capacity in 2031. The share of colocation is expected to drop, although it is still increasing at double-digit rates.

Enterprises’ on-premise datacentre capacity is expected to drop to 19% of the total by 2031, at a rate of about 2% per year, although even here that decline is not so rapid, largely due to the deployment of AI hardware.

Synergy’s data is based on several quarterly tracking research services in hyperscale, colocation and enterprise datacentres, and based on datacentre footprint and operations of the world’s major cloud colocation firms, plus tracking the datacentre hardware market.

John Dinsdale, a chief analyst at Synergy Research Group, said AI is driving the world’s datacentre market towards increased concentration in favour of the hyperscalers.

“Cloud and consumer-oriented digital services have been driving changes in datacentre deployment patterns for many years now, but over the last three years, AI technology has accelerated those changes,” he said.

“We are seeing a different mix of datacentre usage across the regions, but overall, the world is racing towards a situation where hyperscale operators are responsible for the bulk of global datacentre capacity. There are almost 800 hyperscale datacentres in our known future pipeline, enabling hyperscale capacity to double in just three years,” Dinsdale added.

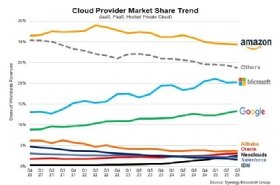

By the third quarter of 2025, worldwide spend on cloud services had reached $107bn, up from $68bn two years before that, in 2023.

Among the big three, Amazon’s market share has been in a state of gradual decline since 2022. In the third quarter of 2025, it had a 29% market share, down from just under 34% in the third quarter of 2022.

Meanwhile, the third-quarter 2025 market share for Microsoft was 20%, and 13% for Google Cloud. Both of these are seeing increases in market share, with Microsoft up from 13% in the fourth quarter of 2020.

Meanwhile, so-called neocloud providers – those that specialise in AI datacentre capacity – have a market share of 2.5%.

Dinsdale said: “Beyond the three market giants, a wide mix of smaller players is competing for traction, but the reality is that third-placed Google remains nearly four times the size of fourth-placed Alibaba, underscoring the widening gulf between the market leaders and the rest of the field.”